Have you ever felt like you’re running on a hamster wheel, working a job you don’t love just to pay the bills, counting down the years—or decades—until you can finally relax? If so, you’re not alone. So, what is the FIRE movement? This comprehensive guide on financial independence retire early explained will break down the benefits of FIRE, explore why you might pursue FIRE, and detail how to achieve financial freedom. It’s a concept that’s catching on like, well, wildfire. The promise of an alternative path, one where you call the shots long before traditional retirement age, is captivating a generation.

The core idea of FIRE isn’t about being lazy or hating work. At its heart, it’s about one thing: choice. It’s about reclaiming your most valuable, non-renewable resource—your time. It’s a radical rethinking of the relationship between work, money, and life itself. But is it just a pipe dream for the privileged few, or is it an attainable goal for the average person? Let’s dive in and find out.

So, What Is the FIRE Movement, Really? A Deep Dive

At first glance, the acronym seems simple enough: Financial Independence, Retire Early. But unpacking those four words reveals a philosophy that’s far more nuanced than just quitting your job to sit on a beach (though that’s certainly an option!). Let’s break down the two core components.

Financial Independence Explained: The “FI” in FIRE

This is the absolute bedrock of the entire movement. Without the “FI,” the “RE” is impossible. So, what does financial independence truly mean?

Financial independence is the state where you have enough income from your investments or passive sources to cover your living expenses without having to work an active job for money.

Think about that for a second. It’s not about being “rich” in the traditional sense of having a mansion and a fleet of sports cars. It’s about reaching a point where your money works for you, instead of you having to work for it. Your investment portfolio—typically made up of stocks, bonds, and real estate—generates enough cash flow to pay for your housing, food, transportation, healthcare, and fun.

This is the ultimate goal. For many, the “Retire Early” part is just a potential, wonderful side effect. The real prize is Financial Independence itself. It means:

- You are no longer dependent on a paycheck.

- You can say “no” to a project, a promotion, or even a whole career path that doesn’t align with your values.

- You have a powerful safety net against job loss, economic downturns, or unexpected life events.

- You own your time.

This state of FI is often called your “crossover point”—the moment the income from your investments crosses over and surpasses your annual expenses. Achieving this is the central mechanical goal of the entire FIRE movement.

The “RE” in FIRE: Is Early Retirement Really the Goal?

This is where the FIRE movement often gets misunderstood. The “Retire Early” part is what grabs the headlines, but for a huge portion of the community, it’s not about a permanent vacation.

For some, yes, it absolutely is. They want to clock out of their high-stress corporate job at 40 and never set foot in an office again. They might want to travel the world, volunteer full-time, or simply enjoy a life of leisure.

But for many others, “retiring” doesn’t mean stopping work. It means retiring from mandatory work. It means having the freedom to pursue work you love, regardless of the paycheck.

- Maybe you’re a software engineer who dreams of opening a small coffee shop.

- Perhaps you’re an accountant who wants to become a high school math teacher.

- Maybe you want to work part-time at a non-profit, write a novel, or start a YouTube channel about woodworking.

These pursuits might not pay the bills on their own, but if you’ve already achieved Financial Independence, it doesn’t matter. The “RE” in FIRE is about having the option to redefine what “work” means to you. It’s about shifting from work-for-survival to work-for-purpose. This is a critical distinction that makes the FIRE lifestyle so appealing.

The “Why” Behind the Blaze: Why Pursue FIRE?

Okay, so we understand the definition. But that doesn’t explain the explosion in popularity. Why are millions of people, from tech workers in Silicon Valley to teachers in the Midwest, suddenly obsessed with this idea? The motivations run much deeper than just money.

The Core Benefits of FIRE: Beyond Just Money

The reasons people chase FIRE are deeply personal, but they often revolve around a few key themes.

1. Freedom and Autonomy: This is the big one. Imagine waking up on a Monday morning and having complete control over your day. No boss to answer to, no meetings to dread, no commute to suffer through. Your time is 100% your own. This autonomy to design your life is perhaps the most powerful driver behind the movement. It’s the freedom to decide where you live, what you do, and who you spend your time with, without being constrained by the need for a salary.

2. Escaping the “Rat Race” and Burnout: Modern work culture can be brutal. Long hours, high pressure, “always-on” expectations, and toxic environments lead to widespread burnout. Many people feel like they’re sacrificing their mental and physical health for a paycheck. Why pursue FIRE? For many, it’s a lifeboat. It’s a tangible plan to escape a system that feels unsustainable and unfulfilling. It’s a way to say, “I refuse to trade the best years of my life for a job that drains my soul.”

3. The Pursuit of Passion and Purpose: We all have things we’d rather be doing. Whether it’s art, travel, community service, starting a business, or simply spending more time with family, our day jobs often leave little time or energy for our true passions. FIRE offers a future where you have decades of healthy, active years to dedicate to what truly matters to you. It’s not about escaping work, but running towards a more meaningful existence.

4. Increased Resilience and Security: Even if you love your job, the world is an uncertain place. Layoffs, recessions, and health crises can upend your life in an instant. The journey to FIRE, by its very nature, builds an incredible financial fortress. Having a high savings rate and a growing investment portfolio means you’re far less vulnerable to life’s curveballs long before you even reach full FI. This peace of mind, often called “F-You Money,” is a massive benefit in itself. It’s the power to walk away from a bad situation without financial ruin.

The Blueprint: How to Achieve Financial Freedom

This all sounds great in theory, but how does it actually work? It’s not magic; it’s math. The path to FIRE is surprisingly simple, though not necessarily easy. It hinges on a few core principles and consistent action. Let’s explore some early retirement strategies.

Step 1: The Mindset Shift and Defining Your “Why”

Before you even touch a spreadsheet, the most important step is a psychological one. You have to shift from a consumer mindset to a producer/owner mindset. This means fundamentally changing your relationship with money. Instead of seeing it as something to be spent, you see every dollar as a seed you can plant to grow your future freedom.

You also need to define your personal “why.” Why are you doing this? Is it to travel? To be with your kids? To escape a job you hate? Write it down. Make it specific. On the days when you’re tempted to splurge or feel like the goal is too far away, this “why” will be your anchor.

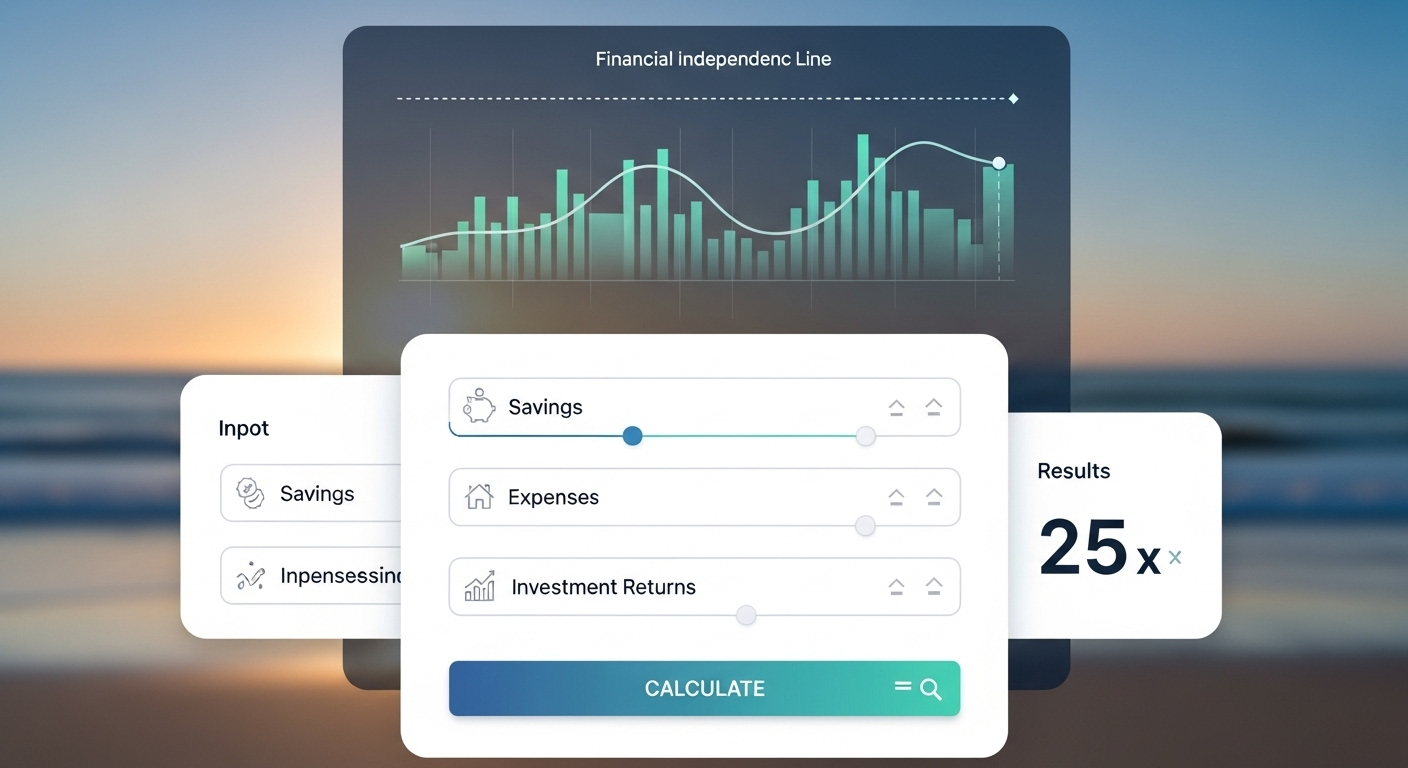

Step 2: Calculate Your Freedom Number (The FIRE Math)

This is where the abstract goal becomes a concrete number. The FIRE community generally relies on a principle called the 4% Rule of Thumb (or the Safe Withdrawal Rate).

The 4% Rule: This rule, based on a famous study called the Trinity Study, suggests that you can safely withdraw 4% of your initial investment portfolio each year (adjusting for inflation) with a very high probability of your money lasting for at least 30 years—and often much longer.

To find your FIRE number, you simply flip this rule on its head:

Your FIRE Number = Your Annual Expenses x 25

That’s it. That’s the target. If you can live on $40,000 per year, your FIRE number is $1,000,000. If you need $80,000 per year, your target is $2,000,000.

Let’s illustrate with a table:

| Desired Annual Spending in Retirement | Multiplied By 25 | Your FIRE Number (Target) |

|---|---|---|

| $30,000 (Lean FIRE) | x 25 | $750,000 |

| $40,000 | x 25 | $1,000,000 |

| $60,000 | x 25 | $1,500,000 |

| $80,000 (Standard FIRE) | x 25 | $2,000,000 |

| $120,000 (Fat FIRE) | x 25 | $3,000,000 |

A quick caveat: The 4% rule is a guideline, not an unbreakable law of physics. Some people prefer a more conservative 3.5% or 3% withdrawal rate (meaning a FIRE number of 28.5x or 33x expenses) for a higher margin of safety, especially for very long retirements. But the 25x rule is the standard starting point.

The most powerful variable in this equation is your annual expenses. Every dollar you cut from your annual spending reduces your FIRE number by $25. This is why a core tenet of the FIRE lifestyle is conscious and optimized spending.

Step 3: Master the Three Levers of Early Retirement Strategies

Once you have your number, there are three main levers you can pull to reach it as quickly as possible. The goal is to maximize the gap between your income and your expenses, and then invest that gap wisely.

Lever 1: Dramatically Increase Your Savings Rate

Your savings rate is the single most important metric on your journey to FIRE. It’s the percentage of your after-tax income that you save and invest. It’s far more powerful than your investment returns, especially in the early years.

Why? Because your savings rate directly determines your working timeline. Think about it:

- If you save 10% of your income, you save 1 year’s worth of expenses every 9 years you work. Retirement is a long, long way off.

- If you save 25% of your income, you save 1 year’s worth of expenses every 3 years you work. Much better.

- If you save 50% of your income, you save 1 year’s worth of expenses for every 1 year you work. You can retire in about 17 years.

- If you save 75% of your income, you save 3 years’ worth of expenses for every 1 year you work. Retirement is less than a decade away.

(These numbers are simplified and don’t include investment growth, which would speed things up even more!)

The average American saves around 5-8%. FIRE chasers aim for 50% or more. This sounds impulsive by conventional standards, but it’s the rocket fuel of the movement. How do they do it? By pulling the next two levers.

Lever 2: Aggressively Optimize Your Spending

This is not about being cheap. It’s about being intentional. It’s not about giving up lattes if they bring you genuine joy; it’s about plugging the massive, often unconscious, spending leaks in your life.

The focus is typically on the “Big Three” expenses, where you get the most bang for your buck:

- Housing: Can you live in a smaller place, get a roommate, “house hack” (buy a duplex and rent one side out), or move to a lower-cost-of-living area? Shaving a few hundred dollars off your mortgage or rent each month is a monumental win.

- Transportation: Do you need two cars? Can you get by with one, or even none? Could you bike to work? Buying reliable used cars instead of new ones can save you tens of thousands of dollars over a decade.

- Food: This is a big one. It’s not about eating ramen noodles every night. It’s about planning meals, cooking at home more often, buying groceries in bulk, and limiting expensive restaurant meals and food delivery to intentional treats.

By ruthlessly optimizing these three categories, you can often free up 20-30% of your income without feeling deprived.

Lever 3: Earn More and Invest the Difference

While cutting expenses is powerful, there’s a limit to how much you can cut. There is, however, theoretically no limit to how much you can earn.

Strategies for this lever include:

- Negotiating your salary: A single 10% raise can be worth tens of thousands of dollars.

- Job hopping: Strategically changing companies every few years is often the fastest way to increase your salary.

- Developing high-value skills: Getting certifications or learning new skills to move into a higher-paying field.

- Starting a side hustle: From freelancing and consulting to driving for a rideshare service or selling crafts on Etsy, a side income can be directed 100% towards your investments, dramatically accelerating your timeline.

The Crucial Final Step: Invest, Invest, Invest

The money you save is your kindling. Investing is the fire that makes it grow. You cannot save your way to FIRE in a 0.1% interest savings account. You need your money to work for you through the power of compound growth.

The go-to investment vehicle for the FIRE community is low-cost, broad-market index funds or ETFs (Exchange Traded Funds).

- Why? Instead of trying to pick winning individual stocks (which is incredibly difficult, even for professionals), an index fund buys you a tiny piece of every company in a major market index, like the S&P 500.

- Benefits: This gives you instant diversification, it’s incredibly low-cost (low fees are critical!), and it allows you to capture the long-term growth of the overall market. It’s a “set it and forget it” strategy that has historically performed very well over the long run.

The strategy is simple: every single month, you automatically invest your saved money into these funds, regardless of whether the market is up or down (this is called dollar-cost averaging). Then, you leave it alone and let it grow.

Not All Fires Burn the Same: Exploring the Different Types of FIRE

The FIRE movement is not a monolith. It’s a spectrum, and people have adapted the principles to fit their own goals and comfort levels. Understanding these “flavors” of FIRE can help you see where you might fit in.

| Type of FIRE | Annual Spending Target (Example) | Key Characteristics & Lifestyle |

|---|---|---|

| Lean FIRE | $25,000 – $40,000 | Extreme frugality and minimalism are key. Often involves living in a very low-cost-of-living area. The goal is to escape the workforce as quickly as humanly possible. |

| Standard/Traditional FIRE | $40,000 – $100,000 | A comfortable, middle-class lifestyle. Not extravagant, but not overly restrictive. This is the most common target. |

| Fat FIRE | $100,000+ | Allows for a more luxurious retirement with frequent travel, expensive hobbies, and high-end living. Requires a much larger portfolio and a longer/higher-earning accumulation phase. |

| Barista FIRE | Varies | You’ve saved enough that you only need a part-time, low-stress job to cover current expenses or, more commonly, to get health insurance. Your investments are left untouched to keep growing. |

| Coast FIRE | Varies | You’ve saved enough in your retirement accounts that, without another contribution, compound growth alone will get you to your traditional FIRE number by a normal retirement age (e.g., 65). This allows you to “take your foot off the gas” and work just enough to cover current expenses. |

Recognizing these different paths is crucial. It shows that how to achieve financial freedom is not a one-size-fits-all formula. You can tailor the journey to your own vision of a good life.

The Unspoken Challenges and Criticisms of the FIRE Lifestyle

It’s easy to get swept up in the excitement, but it’s important to have a clear-eyed view of the potential downsides and critiques. Chasing FIRE is a marathon, not a sprint, and there are hurdles along the way.

1. The Sacrifice Can Be Intense: Achieving a 50%+ savings rate requires significant, sustained sacrifice. It can mean saying “no” to vacations with friends, living in a less desirable area, or driving an old car for years. There’s a real risk of “scarcity mindset” burnout, where you become so obsessed with saving that you forget to live in the present. Finding a balance is a constant struggle.

2. The Math Isn’t Guaranteed: The 4% rule is based on historical data. Future market returns are not guaranteed. A major market crash right after you retire (this is called sequence of returns risk) could seriously impact your portfolio’s longevity. Healthcare costs are another huge, unpredictable variable that could throw a wrench in the numbers.

3. It’s a Path of Privilege: Let’s be honest: it is significantly easier to pursue FIRE if you have a high income, no student debt, and no dependents. For someone earning a median wage while supporting a family, a 50% savings rate is a fantasy. While the principles of spending less than you earn and investing are universal, the speed at which one can reach FIRE is heavily influenced by starting circumstances.

4. The “What Now?” Problem: People spend years, even decades, laser-focused on a single goal: hitting their number. What happens the day after they quit their job? Many early retirees report feeling a sense of loneliness, boredom, and a loss of identity and purpose. Your job, for better or worse, provides structure, social connection, and a sense of contribution. Rebuilding that from scratch in retirement is a real and often overlooked challenge of the FIRE lifestyle.

Conclusion: Is Chasing FIRE Right for You?

So, after all this, we return to the central question: What is FIRE and why are so many people chasing it?

The FIRE movement, at its core, is a response to a deep-seated human desire for control over our own lives. It’s a framework for turning a vague dream of “freedom” into a concrete, actionable plan. It’s a rejection of the default path—work for 40-50 years, save a little, and hope you have enough health and energy left to enjoy a decade or two of retirement.

It’s not a perfect system, and it’s not for everyone. The journey demands discipline, sacrifice, and a willingness to be different. But the beauty of FIRE is that you don’t have to reach the finish line to win.

Every step you take on the path—every dollar you save, every debt you pay off, every investment you make—buys you a little more freedom. It builds your resilience. It gives you options. Maybe you don’t reach full FIRE at 40, but you build enough of a cushion to take a six-month sabbatical, switch to a less stressful career, or go part-time to be with your family.

That, ultimately, is the real power of this movement. It’s not just about financial independence retire early explained as a destination; it’s about the empowerment and security you build along the way. It’s about asking yourself what you truly want out of life and then having the courage, and the financial means, to go out and build it.

Add your first comment to this post